By: Mukasiri Sibanda* (Guest Blogger)

In Zimbabwe, Mining Agreements (MAs) or contracts are not publicly available and accessible. This is so despite that constitutionally speaking; minerals are public assets and must be publicly accounted for. Secretive MAs may have harmful tax incentives which may prejudice mineral revenue flows to the public purse and consequently inhibit broad based socio-economic development.

In 2014, Zimbabwe was ranked 156 out of 175 countries on Global Corruption Perception Index released by Transparency International. Given such high levels of corruption in the country, the secrecy surrounding MAs presents opportunities for corrupt public official and corporates to benefit at the expense of the nation. Secretive MAs have been identified as one of the causes for the failure of resource rich countries to leverage on natural resources to attain socio-economic transformation that lifts the poor out of poverty.

The news surrounding the tax dispute between Zimbabwe Platinum Mines (ZIMPLATS) and the Zimbabwe Revenue Authority (ZIMRA) clearly demonstrates the imperative for full disclosure of mining contracts or mining agreements. Zimplats is one of the largest platinum mining companies in Zimbabwe and operates out of Mhondoro-Ngezi. The company is listed on the Johannesburg and Australian Stock Exchanges and is largely owned by Implats. A local weekly newspaper, the Financial Gazette, carried a story on 26 February titled “ZIMPLATS Wins Tax Dispute”.

According to the story, ZIMPLATS entered into a Mining Agreement (MA) with government in 1994 which stipulated that royalty rates will be paid at 2.5% of fair market values. Further, the MA exempted ZIMPLATS on payment of Additional Profit Tax. These fiscal incentives are known as stabilisation clauses which are used as a tool to attract investments in a sector through the insulation of tax incentives from potential future changes in legislation.

ZIMRA argued that the MA agreement clause on stable 2.5% royalty rates was not binding since requisite Statutory Instrument (SI) was not issued as stipulated by the Income Tax Act (Chapter 23:06) whereas Zimplats argued otherwise (case number 12292/11). Justice Lavender Makoni in favour of Zimplats citing that “the definition of taxes under Income Tax Act (Chapter 21:05) does not include royalties under the Mines and Minerals Act (read with Chapter VII of the Finance Act (Chapter 23:04).

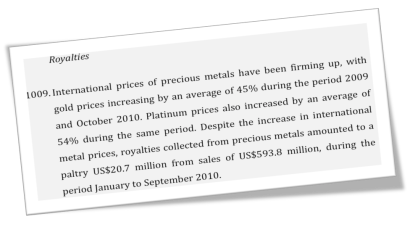

The period under consideration in this dispute is 1 January 2004 to 30 September 2010. ZIMPLATS argued that it had paid royalty rates at 3% and 3.5% which were above the stipulated 2.5% in its MA with government. The overpayment amounted to US$6,057,146.00. It must be noted that royalty fees for platinum have since been further repeatedly revised upwards to 5% on1 January 2011 and 10% on 1 January 2012. Experts estimate that ZIMPLATS may claim up to US$120 million from ZIMRA. It is, however, noteworthy that ZIMRA has been complying with the reviewed royalty rates and has not demanded restitution as Justice Lavender Makoni noted in her judgement.

On another separate note the dispute between ZIMRA and ZIMPLATS on Additional Profit Tax (APT) payment amounted to $50.4 million from 2002 to 2011.

These stabilisation clauses pertaining to flat royalty rates of 2.5% and the waiver of APT when added up shows that the public purse is at risk of losing over $176million. This becomes glaring when one considers the 2011 national budget statement which lamented poor royalty revenues despite booming mineral prices.

It is interesting to note that the MA that ZIMPLATS had with government was concluded in 1994. During this period, agriculture and manufacturing were the mainstay sectors of Zimbabwe’s economic growth. This has since changed as mining is now the lead economic sector after surpassing agriculture and manufacturing based on its contribution to both the Gross Domestic Product (GDP) and export earnings.

The country’s 5 year (2013-2018) economic blueprint, the Zimbabwe Agenda for Sustainable Socio Economic Transformation (ZimAsset) is anchored on judicious exploitation of mineral assets. Yet MAs that were entered into over 2 decades ago are likely to encumber whatever plans are in place of fully capturing mineral resource rents and fully beneficiating the country’s mineral assets. These unbeneficial tax incentives should be put in the context of the fact that mineral resources are wasting assets that cannot be recovered once exploited. In addition, the failure to judiciously exploit the country’s mineral resources means that treasury is starved of much needed revenue and this has the knock-on effect of stifling much needed investments in creating social safety nets to ameliorate the plight of many poor Zimbabweans.

Reviewing of MAs to unlock the mining sector’s potential in line with the new economic status of mining is critical to the realisation of ZimAsset’s transformation agenda. MAs should be publicly accessible and it is disheartening to note that the details of the much touted recent $3 billion platinum MA between Russian investors and government are not public. Do we have to wait for disputes to start exposing the malcontents of this MA as is the case with Zimplats? Zimbabwe should follow the lead of countries such as the DRC and Guinea in publishing mining contracts or mining agreements. This helps plug opportunities for corruption and ensures that public officials negotiate in good faith knowing full well that the mining agreements will be subjected to public scrutiny.

* Mukasiri Sibanda is an Economic Governance Officer at the Zimbabwe Environmental Law Association ( a member of Publish What You Pay Zimbabwe)